What is Altman Z Score For Risk Assessment in Banks ?

2 minutes read

Altman Z Score is used to identify bankruptcy potential of the firms or companies. The Altman score is the output of a credit strength test for determining whether a company, notably in the manufacturing space, is headed for bankruptcy. However, the initial model developed by Altman does not help in predicting bankruptcy of banks. For that, we need to use Altman’s customized model for banks.

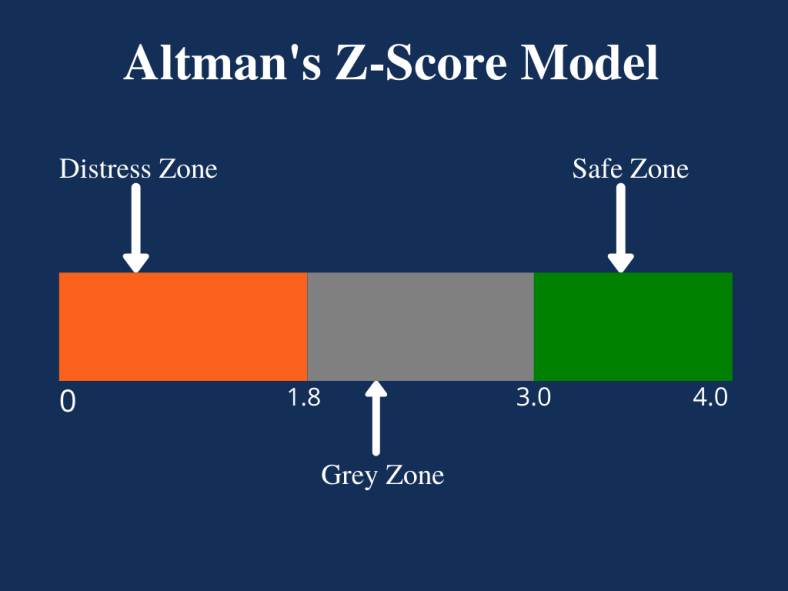

This is a Credit Risk Assessment model. NYU Stern Finance Professor Edward Altman developed the Altman score formula in 1967, and it was published in 1968. The Altman Z-score is the output of a credit strength test for determining whether a company, notably in the manufacturing space, is headed for bankruptcy. The formula takes into account profitability, leverage, liquidity, solvency, and activity ratios. An Altman Z-score close to „0‟ suggests a company might be headed for bankruptcy, while a score closer to „3‟ suggests a company is in solid financial positioning.

Altman Z-Score = 1.2A + 1.4B + 3.3C + 0.6D + 1.0E

Where;

A = working capital / total assets

B = retained earnings / total assets

C = earnings before interest and tax / total assets

D = market value of equity / total liabilities

E = sales / total assets

A score below 1.8 means it’s likely the company is headed for bankruptcy, while companies with scores above 3 are not likely to go bankrupt. In more recent years, however, it was suggested that, a Z-Score closer to 0 indicates a company may be in financial trouble.

The bankruptcy is calculated on following parameters :

- Working capital/total assets

- Retained earnings/total assets

- EBIT/total assets

- MV of equity/BV of debt

Also – Calculate Debt to Equity Ratio for Loan Processing, Formula

Leave a Comment