Does Gratuity and PF Taxable ?

2 minutes read

Does Gratuity and PF Taxable ? – Whether Gratuity paid to the employees on retirement or leaving the jobs are taxable as per Income Tax rule ?

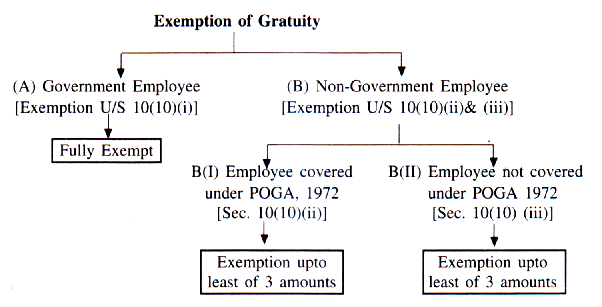

As per the existing law Government employee Gratuity and PF (Provident Fund) receipts on retirement are exempt from tax. In the hands of non-Government employee, gratuity is exempt subject to the limits prescribed in this regard and PF receipts are exempt from tax, if the same are received from a recognized PF after rendering continuous service of not less than 5 years.

Read Also : Whether Provident Fund Taxable ?

As per the Income Tax rule of Section Sec. 10(10)):

(i) Any death cum retirement gratuity received by Central and State Govt. employees, Defence employees and employees in Local authority shall be exempt.

(ii) Any gratuity received by persons covered under the Payment of Gratuity Act, 1972 shall be exempt subject to following limits:-

(a) For every completed year of service or part thereof, gratuity shall be exempt to the extent of fifteen days Salary based on the rate of Salary last drawn by the concerned employee.

(b) The amount of gratuity as calculated above shall not exceed Rs 10 Lakh.

(iii) In case of any other employee, gratuity received shall be exempt subject to the following limits:-

(a) Exemption shall be limited to half month salary (based on last 10 months average) for each completed year of service

(b) Rs. 10 Lakhs whichever is less. Where the gratuity was received in any one or more earlier previous years also and any exemption was allowed for the same, then the exemption to be allowed during the year gets reduced to the extent of exemption already allowed, the overall limit being Rs. 10 Lakhs.

As per Board’s letter F.No. 194/6/73-IT(A-1) dated 19.6.73, exemption in respect of gratuity is permissible even in cases of termination of employment due to resignation. The taxable portion of gratuity will quality for relief u/s 89(1). Gratuity payment to a widow or other legal heirs of any employee who dies in active service shall be exempt from income tax(Circular No. 573 dated 2 1.8.90).

Leave a Comment